FI Insights: Banks and FIs are increasingly joining the BNPL race.

The pandemic era injected new urgency into digital banking shifts.

For installment style credit products in particular, physical constraints

and financial insecurities fast-tracked both consumer interest and

available offerings.

The rise of BNPL is widely reported, although discussions profile a few early fintech providers. Based on survey responses, we now expect a wave of banks and FI participants.

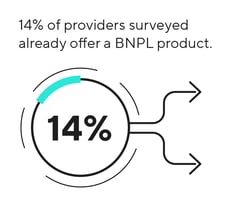

Across the digital banking, fintech, and FI landscape, 14% of providers

Across the digital banking, fintech, and FI landscape, 14% of providers

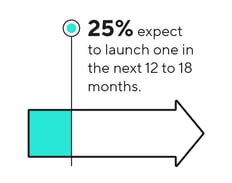

surveyed already offer a BNPL product. Of those that do not currently have one, 25% expect to launch one in the next 12 to 18 months.

Notably, the largest institutions display the most go-to-market zeal.

For enterprises with over $50 billion assets under management (AUM), 47% revealed plans to launch BNPL within 18 months.

With respect to BNPL, banks stand to lose up to $10 billion in annual revenues to the ever-expanding roster of merchant-centric fintechs. McKinsey suggests that inadequate response to consumer and merchant demands for flexible, point-of-sales payment options simply gives market share away to more agile enterprises.

According to Fifth Third’s Dervan, customer-centered banks “have

an obligation to build compelling experiences and meet customers in

the channel of their choice.”

For many banks, he reminds, this means “figuring out ways to operate

internally in product territories that aren’t as well-traveled.”

Despite new market participants, worries and inflexibility sideline

some.

Despite the uptake to date, BNPL still concerns some banks and FIs.

In response to the question “What internal constraint or conflict

is prohibiting you from launching a BNPL or installment-credit

product?” responses included:

-

“Market maturity, collection infrastructure, and regulations”

-

“The right technology and/or partner”

-

“Finding the right user experience”

-

“Resources and technology”

-

“IT bandwidth”

Certainly, BNPL may not fit the risk criteria or customer profile of every bank and financial institution. However, industry interviewees challenged cautious enterprises to reframe the opportunity of BNPL and emerging digital products.

“Don’t wait until the majority of your customer base wants a product before launching,” guides WestCap’s Mokhat. “Those that want it, will find it, and they’ll find it with someone else. This is a Trojan Horse moment – the competitor that just gave your customer a great BNPL experience will then offer them a deposit account, a loan, and a credit card.”

According to Mokhat, meeting customers’ evolving needs is what really matters. Think about lifetime value differently, or you’ll wake up one day and your customers will be gone.

"Meeting customers' evolving needs is what really matters. Think about lifetime values differently, or you'll wake up one day and your customers will be gone."

- Kapil Mokhat, Managing Director, WestCap

Practically, this requires recognizing the shortcomings of inefficient, inflexible legacy infrastructure and reconsidering traditional product launch pathways – especially those that drain internal resources.