The Rise of Embedded Finance Signals Growth for FinTech

With Google adding checking accounts, Apple entering the credit card arena, and Amazon offering loans at the point-of-sale, the trend is clear—non-traditional finance players are making a big push for market share in consumer financial services.

But how can these tech giants pivot so swiftly into an industry that has been dominated by traditional players for decades?

The answer lies in the rise of embedded finance.

What is embedded finance?

Embedded finance is the seamless integration of financial services within the product offerings of non-financial businesses. For example, if you’re shopping for home-workout equipment, the retailer may enable you to finance the purchase within the checkout experience.

The goal of these businesses offering embedded finance is not necessarily to compete directly with banks on their turf. Instead, it offers an opportunity for smart players to diversify revenue streams and increase customer lifetime value. Ultimately, it’s about meeting the needs of the modern consumer in a digital world.

The origins of embedded finance

Superapp platforms in Southeast Asia seemingly perfected the process of embedded finance early on. These platforms have seen tremendous success building interconnected systems of money movement that link a consumers’ wallet directly to in-app services. By leveraging the power of open banking, e-commerce, food delivery, transportation, utilities payment, and even insurance products can meet consumer needs in an effective way.

Ride sharing platform Grab recently expanded their financial solutions with a “buy now, pay later” solution, a micro-investment platform, and a consumer loan product — all are accessible in one app. Given that Grab is already so deeply integrated within the lives of its existing consumers, the push towards embedded finance naturally increases its customers’ usage as a one-stop-shop platform layered with financing capabilities.

Embedded financing evolving in the US

While consumer behaviors may differ in Asia and the United States, big tech players and SaaS providers in the US are well-positioned to recreate some of this secret sauce.

Large merchant and consumer networks are sitting on a trove of valuable data that can easily translate into increased engagement and lower customer acquisition costs. Many of these tech giants have already started to explore partnerships with banking-as-a-service (BaaS) providers to navigate the infrastructure and regulatory complexities of financial services.

Let’s take a deeper look at how these tech giants are evolving to meet the needs of the modern consumer.

E-commerce marketplace

Amazon, one of the most identifiable brands in the world has started to dive head-first into the embedded finance space by offering the following:

Amazon Pay: An e-wallet that allows consumers to checkout via their Amazon account

Amazon Lending: A credit line designed for merchants on their platform, in partnership with Goldman Sachs’ Marcus brand

Amazon Card: A co-branded credit card for consumers, in partnership with Synchrony Bank and Chase

A SaaS e-commerce enabler

Shopify continues to make waves as they threaten to disrupt almost every industry that is tangentially related to e-commerce. Recently, they have made a big push into embedded finance, including:

Shopify Capital: A small business loan product for merchants on their platform

Shop Pay Installments: A point-of-sale financing product, in partnership with Affirm

Shopify Balance: A bank account for merchants on their platform to consolidate all their cash flows in one place

A ride sharing application

Despite Uber’s up-and-down year, they continue to make a push into embedded finance.

Uber Money: A debit card and and bank account for drivers integrated directly into the Uber Driver app, in partnership with GreenDot

Uber Card: A credit card for consumers, in partnership with Barclays

The future of embedded finance

In this growing digital economy, the rise of embedded finance highlights a somewhat inconvenient truth. Many consumer-facing tech companies could be capable of competing with incumbents in the financial industry.

To date, partnership remains the dominant go-to-market model with tech driving the bus and financial institutions providing the fuel. However, smart financial institutions will be carefully watching this trend and must remain flexible to avoid future disintermediation. Expect to see a higher adoption of embedded finance among direct-to-consumer companies with the continued expansion of FinTech across all verticals.

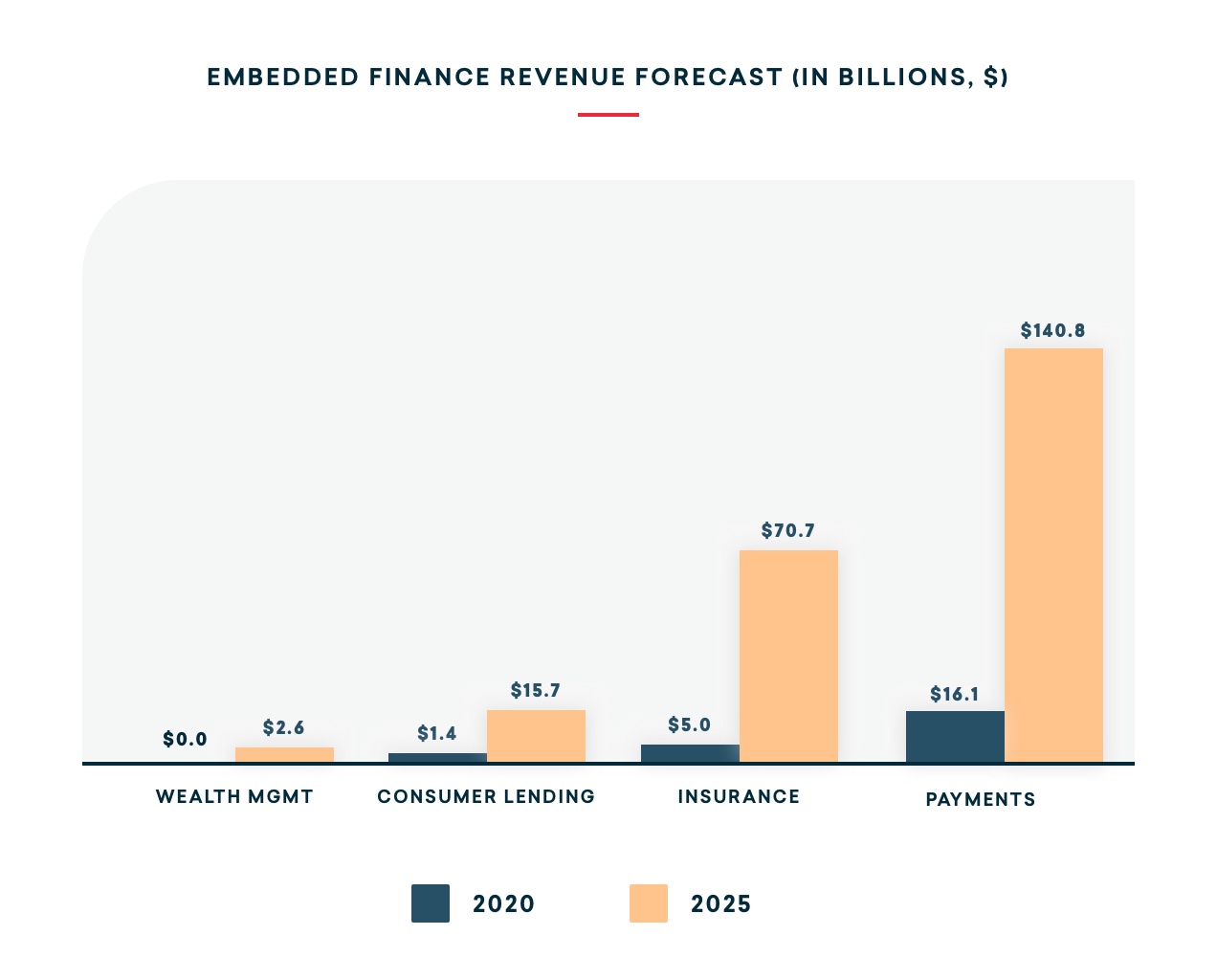

There is a meaningful opportunity for many direct-to-consumer companies to offer financing products into their existing platforms, instead of reselling them. A recent report predicts that the revenue gains from the embedded finance market will see a ten-fold increase from $22.5B in 2020, to $230B in 2025.

Source: Lightyear Capital

Alex Johnson of FinTech Takes suggests that the key strategy is for embedded finance to be integrated within the right context of the consumer’s path of engagement on the platform. For example, a consumer looking for financing options at checkout would find a “pay over time” installment offer significantly more appealing than being redirected to another site to apply for a loan.

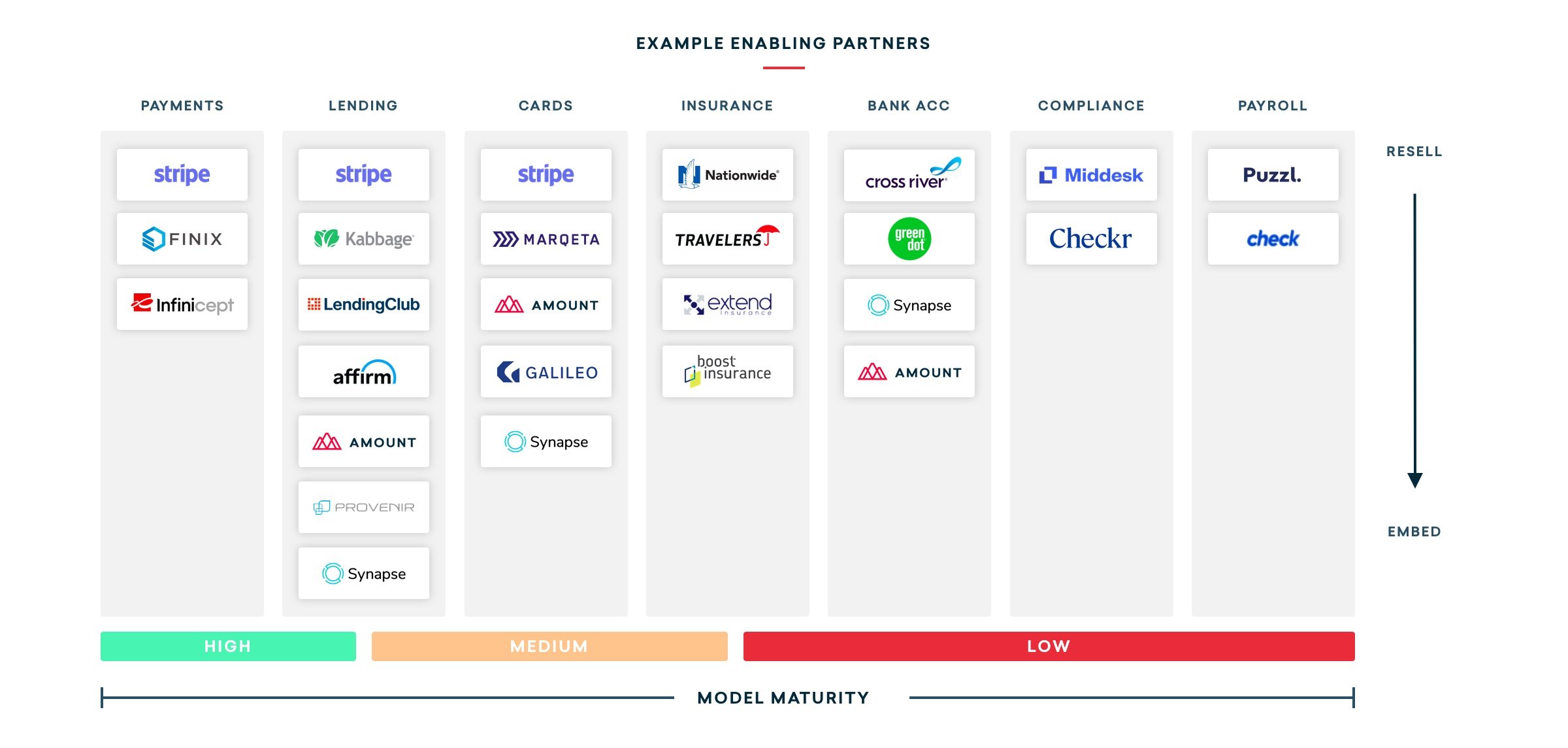

While some businesses may choose to build out their own financial services in-house, others will be deterred by the burden of regulation, infrastructure, and operations that exists in finance. This presents a golden opportunity for FinTechs, with their technological capabilities, to partner with these businesses to embed value to their end users’ customer journeys.

Source: Andreessen Horowitz

What does this mean for your financial institution?

The growth and maturation of Banking-as-a-Service (BaaS) will be one of the core drivers of the embedded finance movement going forward. Providers that can offer partners an effective toolkit to connect with core systems and configure financial elements into their customer experiences will see their total addressable market expanded materially. For now, the partnership model is out of the gates with a lot of momentum. The key is to find a technology provider that orchestrates a user-centered customer experience with back-end technology built for the biggest banks and financial institutions in the world.